Personal loan consolidation is like putting on a superhero cape for your finances—suddenly, you feel invincible against the mountain of debt looming over you! This process allows you to bundle multiple loans into one neat package, making your financial life as tidy as a cat in a sunbeam. Imagine waving goodbye to the chaos of various interest rates and payment dates, and saying hello to a single, manageable monthly payment!

But wait, there’s more! Not only can personal loan consolidation simplify your life, but it can also save you money over time. Think of it as upgrading from a rusty old bicycle to a shiny new car—smoother rides and fewer bumps along the way. So, buckle up as we explore the ins and outs of this financial strategy, making sure to steer clear of any potholes that might come your way!

Understanding Personal Loan Consolidation

Personal loan consolidation may sound like a fancy term that belongs in a financial textbook, but it’s really just a way of simplifying your life one loan at a time. Imagine juggling too many balls in the air; eventually, something’s bound to drop. That’s where loan consolidation steps in—like a superhero with a budget cape, swooping in to rescue you from the chaos of multiple payments and interest rates.Personal loan consolidation involves combining multiple loans into a single one, ideally with a lower interest rate.

This not only lightens your monthly payment load but also makes it easier to manage your finances. Think of it as a financial spring cleaning—clearing out the clutter and replacing it with one shiny, manageable loan. Not only can this help reduce your monthly payments, but it can also improve your credit score if you handle it correctly.

Benefits of Personal Loan Consolidation

Consolidating your loans can lead to several advantages that can make your financial journey smoother. Here are some noteworthy benefits you might want to consider:

- Lower Monthly Payments: By securing a loan with a lower interest rate, you can significantly reduce your monthly payment burden. It’s like trading in your gas-guzzling SUV for a fuel-efficient hatchback.

- Single Payment: Instead of managing multiple loans and their respective due dates, you’ll only need to remember one! Your brain will thank you for lightening the load.

- Potential Improvement in Credit Score: If you manage to pay down your loans with the new consolidated loan, your credit utilization ratio could improve, and who doesn’t love a shiny credit score?

- Fixed Interest Rates: Many consolidation loans offer fixed rates, meaning your payment won’t change over time, allowing for better financial planning. It’s like having a predictable friend—less drama!

The Process of Consolidating Personal Loans

Getting from scattered loans to a streamlined single loan doesn’t happen with a snap of your fingers; it’s a process that involves several crucial steps. Here’s how to navigate this financial maze effectively.

1. Assess Your Current Loans

Take a hard look at your existing loans, including interest rates and monthly payments. Knowing where you stand is like checking your bank account before a shopping spree—essential for avoiding regret!

2. Research Consolidation Options

Shop around for lenders offering consolidation loans. Compare interest rates, fees, and repayment terms. This is your time to channel your inner financial detective—magnifying glass and all!

3. Apply for a Consolidation Loan

Once you’ve found the right fit, apply for the loan. Be prepared with documentation like income statements and credit reports—think of it as gathering your homework before a pop quiz.

4. Pay Off Existing Loans

Once your consolidation loan is approved, use the funds to pay off your multiple loans. Like the grand finale of a fireworks show, this step is where the real magic happens!

5. Stay on Top of Payments

Commit to paying your new loan on time every month. Set reminders, enroll in automatic payments, or use a calendar app. After all, you don’t want to slip back into the chaos of missed payments!

Common Pitfalls to Avoid During Personal Loan Consolidation

While personal loan consolidation can be a lifebuoy in a sea of debt, there are some common missteps that could lead to an unintended dive into deeper waters. Here are key pitfalls to watch out for:

- Ignoring the Fine Print: Before signing anything, make sure to read the terms and conditions. Hidden fees and clauses can be lurking like a villain in the shadows!

- Choosing the Wrong Lender: Not all lenders are created equal. It’s important to select one who offers favorable terms and a good reputation. Take recommendations from friends or do some online research.

- Extending the Loan Term: While a lower monthly payment sounds great, extending the loan term can lead to paying more interest in the long run. It’s like trading a short walk for a long hike; it’s all about the journey!

- Accumulating More Debt: Resist the urge to rack up new debt while paying off the consolidation loan. It’s a slippery slope that can lead back to square one—debt city!

Financial Strategies Related to Personal Loan Consolidation

Navigating the winding roads of personal loan consolidation can be as tricky as finding a parking spot at a crowded mall on Black Friday. But fear not, for savvy financial strategies are your trusty GPS, guiding you to a smoother financial journey. Here, we delve into managing your finances before and after loan consolidation, compare it with other debt management strategies, and highlight the indispensable role of credit counseling.

Buckle up!

Managing Finances Pre and Post Consolidation

Successfully managing your finances surrounding personal loan consolidation is akin to preparing a gourmet meal; it requires the right ingredients, timing, and a pinch of finesse. Here are some essential tips to help you whip up a financial feast:

- Assess Your Financial Situation: Before consolidating, gather your bills like you’re collecting Pokémon cards. Know what you owe, interest rates, and payment schedules.

- Create a Budget: A budget is your financial map. Detail your income, expenses, and savings goals. It’s like your financial compass, pointing you toward fiscal North!

- Set Savings Goals: Aim to save a little every month! Think of it as your financial cheerleader, rooting for a future where you can splurge without guilt.

- Monitor Your Credit Score: Keep an eye on your credit score like it’s a reality TV show. You want the drama, but not too much; ideally, it should trend upwards!

- Build an Emergency Fund: Life is unpredictable—like a cat on a hot tin roof. Set aside 3-6 months of expenses to handle unexpected financial surprises.

- Stay Disciplined Post-Consolidation: After consolidating, maintain those smart financial habits. Avoid the urge to go on a shopping spree; remember, “Treat Yo’ Self” only applies to budgeted fun!

Comparison with Other Debt Management Strategies

While personal loan consolidation can be a superhero in your financial saga, it’s crucial to compare it with other debt management strategies that might suit your unique situation. Each tactic has its own flair:

| Strategy | Pros | Cons |

|---|---|---|

| Personal Loan Consolidation | Single payment, potentially lower interest rates, simplified repayment. | May require good credit, fees can apply, and it doesn’t eliminate debt. |

| Credit Card Balance Transfer | Low or no introductory rates, can improve cash flow. | Higher interest rates after intro period, may incur transfer fees. |

| Debt Management Plan (DMP) | Professional guidance, lower interest rates, and fees. | May impact credit score, requires discipline to adhere to the plan. |

| Debt Settlement | Can reduce total debt, may resolve debt quickly. | Significantly impacts credit score, and may have tax implications. |

The Role of Credit Counseling in Personal Loan Consolidation

Credit counseling is like having a seasoned coach in your corner, helping you tackle the financial game. Engaging with a credit counselor can greatly enhance your personal loan consolidation experience by offering tailored advice and strategies that suit your financial circumstances. Here’s how they can help:

- Personalized Financial Assessment: Credit counselors assess your overall financial health, giving you insights into where you stand and what steps to take next.

- Debt Management Plans: They can help create DMPs that may consolidate your debts into a single monthly payment at a lower interest rate.

- Financial Education: Counselors provide resources and workshops to improve your financial literacy—think of it as a financial masterclass!

- Negotiation Assistance: They can negotiate with creditors on your behalf, potentially securing lower interest rates or waiving fees.

- Support and Accountability: Having someone in your corner helps maintain motivation and accountability; every financial victory feels sweeter when shared!

“Consolidation is not just about merging loans; it’s about merging your financial freedom with smart strategies and professional guidance.”

Exploring Related Financial Concepts

Personal loan consolidation is like that friend who offers to grab your scattered notes and organize them into a neat binder. But wait, there’s more! As we dive into the world of financial strategies, we’ll discover how personal loan consolidation relates to debt relief programs, pit home equity loans against personal loan consolidation, and even navigate the labyrinth of estate planning while juggling personal loans and debts.

So, fasten your seatbelts as we explore these exciting financial avenues!

Relationship Between Personal Loan Consolidation and Debt Relief Programs

Personal loan consolidation and debt relief programs are two financial superheroes, both fighting the evil villain named Debt. While personal loan consolidation involves pooling multiple debts into one manageable loan, debt relief programs typically aim to reduce the overall amount owed through negotiation or settlement. Here’s how they compare in the battle for financial freedom:

- Consolidation: Combines various debts into a single loan with a potentially lower interest rate.

- Debt Relief Programs: Negotiate with creditors to reduce the total debt amount, often leading to a lump-sum settlement.

- Impact on Credit Score: Consolidation can improve your credit score over time if payments are made on time, while debt relief can initially harm your score but may improve it in the long run as debts are resolved.

- Duration: Personal loan consolidation is typically a longer-term solution, whereas debt relief programs can provide quicker relief but might require a few years of commitment.

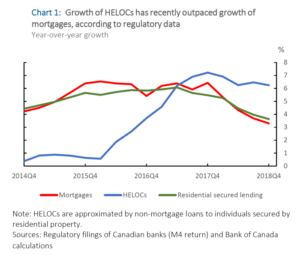

Comparison of Home Equity Loans Versus Personal Loan Consolidation

When weighing home equity loans against personal loan consolidation, envision a classic showdown between two heavyweights in the financial arena. Both have their merits and pitfalls, but they cater to different needs and risk appetites. Let’s break it down:

- Collateral: Home equity loans require your home as collateral, making it a riskier option. On the other hand, personal loan consolidation is typically unsecured, meaning no collateral is needed.

- Interest Rates: Home equity loans often come with lower interest rates, making them attractive for larger debts. Personal loan consolidation rates can vary widely based on creditworthiness.

- Usage Flexibility: Home equity loans are usually earmarked for home improvements or major expenses, whereas personal loan consolidation can be used for various debts.

- Loan Amounts: Home equity loans generally offer larger amounts, while personal loan consolidation is often limited by your credit score and income.

Guide to Effective Estate Planning While Managing Personal Loans and Debts

Estate planning is a bit like preparing for a financial scavenger hunt: you want to make sure that everything is in order for the future while managing the present. Effective estate planning while juggling personal loans and debts requires a bit of finesse and foresight. Here’s a roadmap to guide you through it:

- Inventory Your Assets: List your assets, including any personal loans. Knowing what you have (and owe) is essential for crafting an effective estate plan.

- Prioritize Debts: Determine the priority of your debts. High-interest debts should be tackled first to avoid them overshadowing your estate.

- Consider Life Insurance: Having a life insurance policy can help cover debts after you’re gone, relieving your heirs of financial burdens.

- Consult with Professionals: Engage with financial advisors or estate planners to ensure your debts are managed and your estate is protected. They can provide personalized strategies tailored to your situation.

“Good estate planning is like a financial GPS; it helps you navigate through the complexities of debt while ensuring your legacy is left intact.”

End of Discussion

As we wrap this financial adventure, remember that personal loan consolidation isn’t just about combining debts; it’s about taking control of your financial destiny! By understanding the benefits, avoiding common mistakes, and managing your finances wisely, you can transform your monetary mayhem into a harmonious symphony of payments. So, whether you’re ready to consolidate your loans or just kicking the tires, know that your journey to financial freedom is just a decision away!

FAQ Compilation

What is personal loan consolidation?

Personal loan consolidation is the process of combining multiple loans into one single loan to simplify payments and potentially reduce interest rates.

How does personal loan consolidation affect my credit score?

While consolidating can initially lower your score due to inquiries, making timely payments can improve your score over time.

Can I consolidate loans if I have bad credit?

Yes, but your options may be limited and could come with higher interest rates. It’s best to shop around!

Is it better to consolidate or refinance?

Consolidation combines loans into one, while refinancing replaces your existing loan with a new one, often with different terms. The best choice depends on your financial situation.

How long does the consolidation process take?

The consolidation process can take anywhere from a few days to a few weeks, depending on the lender and your preparedness.