Imagine if your credit score was a superhero, swooping in to save your financial day—but alas, it often ends up on the couch binge-watching reality TV instead! Avoid credit mistakes is your ultimate guide to turning that couch potato into a caped crusader. With a sprinkle of savvy strategies and a dash of clever planning, we’ll make sure your credit doesn’t become the villain of your financial story.

From mastering credit management strategies to exploring debt solutions that could rival your favorite superhero team-up, this guide is packed with tips on how to navigate the treacherous waters of credit management. Buckle up as we explore the avenues that lead to a healthy credit score, debt relief options, and financial planning that turns dreams into reality.

Credit Management Strategies

Managing credit can often feel like juggling flaming torches—exciting but risky if you’re not careful. Luckily, avoiding credit blunders doesn’t require a circus act. With the right strategies, you can keep your financial flame bright without getting burned. Here’s a guide to help you sidestep the common pitfalls of credit management and maintain a healthy financial future.

Avoiding Common Credit Mistakes

When it comes to credit management, knowledge is your best friend. Here are effective methods that can keep you from making those dreaded credit mistakes that can haunt your financial history.

- Pay Bills on Time: Late payments are like that clingy ex you just can’t shake off—difficult to get rid of and they leave a lasting impression on your credit score.

- Keep Credit Utilization Low: Aim to use less than 30% of your available credit. Think of it as a fashion statement; you want to look effortlessly stylish, not like you just raided a clearance sale!

- Limit New Credit Applications: Each application can ding your score a little. It’s smart to be selective—like dating, not every credit offer deserves your time.

- Check Your Credit Report Regularly: Make it a habit to review your credit reports. Think of it as checking for hidden monsters under your bed—better safe than sorry!

Credit Counseling Services

Credit counseling services can be a lifesaver for those feeling overwhelmed by their finances. These professionals provide guidance, support, and a roadmap to help you navigate your credit landscape effectively.Credit counselors often provide personalized plans based on your financial situation. They can help you create a budget, set realistic goals, and even negotiate with creditors on your behalf. Imagine them as your financial GPS, always recalculating your route to avoid those pesky credit potholes.

Maintaining a Healthy Credit Score

A healthy credit score is like a VIP pass in the financial world. It opens doors to lower interest rates and better loan terms, making it essential to keep that score shiny and bright. Here are some practical tips to ensure your score stays in the green zone.

- Diversify Your Credit Mix: Having a mix of credit types—like credit cards, auto loans, and mortgages—can bolster your score. It’s like having a well-rounded diet; a little variety goes a long way!

- Set Up Automatic Payments: Automate your payments to avoid late fees. It’s like having a personal assistant reminding you it’s time to pay up—without the awkward small talk.

- Be Cautious with Credit Limits: When requesting credit limit increases, think twice. Too much available credit can lead to temptation. Use your limits wisely, like that last slice of pizza you’re saving for a special occasion.

“Your credit score is your financial reputation, treat it with the care it deserves.”

Debt Solutions and Relief

If debt was a person, it would be that overly clingy friend who just won’t take a hint. But don’t worry, there’s a way to gracefully extricate yourself from this sticky situation! Let’s dive into the world of debt solutions and relief, where we’ll explore how you can reel in your financial waywardness and avoid future credit conundrums. Spoiler alert: it involves a little strategy and a lot of common sense!

Debt Consolidation Strategies

Debt consolidation is like asking your scattered bills to form a well-organized conga line instead of having them chaotically dance around your bank account. By combining multiple debts into one, you can simplify your financial life and potentially lower your monthly payments. Think of it as trading in your old clunkers for a shiny new car—no more mystery noises or unexpected breakdowns! Here are some popular methods:

- Personal Loans: These can help pay off high-interest debts, allowing you to focus on a single monthly payment with a lower interest rate.

- Balance Transfer Credit Cards: Move your high-interest credit card debt to a card with a 0% introductory rate. Just make sure to pay it off before the rate shoots up!

- Home Equity Loans: If you own a home, you can tap into its equity to pay off debts. Just remember, a home is not a piggy bank, so tread lightly!

Following a consolidation strategy can prevent future credit mishaps by ensuring you don’t have multiple due dates and interest rates to juggle.

Debt Management Plans

Debt management plans (DMPs) are like having a personal trainer for your finances, guiding you through a customized workout to shed those pesky debts. A credit counseling agency typically sets them up, and they can help you negotiate lower interest rates and monthly payments with your creditors. Here’s why they can be effective:

- One Monthly Payment: Instead of paying several creditors, you’ll make one payment to the agency, which will distribute it to your creditors.

- Lower Interest Rates: The agency may negotiate better terms on your behalf, saving you money in the long run.

- Credit Score Improvement: As you pay off your debts on time, your credit score can improve, putting you back in the financial fast lane!

DMPs are not a magic wand but rather a structured path to getting your financial health back on track.

Benefits of Debt Relief Options

Debt relief options are akin to finding the secret exit in a video game—suddenly, you realize there’s an easier way out than battling those relentless monsters of interest rates! These options can offer substantial benefits, letting you breathe easier and find financial peace. Here are some major perks:

- Reduced Debt Amount: Some debt relief options allow you to settle your debts for less than you owe, saving you a chunk of change.

- Improved Cash Flow: By reducing monthly payments or the total amount owed, you can free up funds for essentials or savings.

- Less Stress: The weight of financial burdens can be heavy; relieving some of that weight can improve mental health and overall well-being.

Consider these benefits in your journey to financial freedom and watch as your worries begin to fade away like a bad haircut!

Financial Planning and Investments

In the bustling bazaar of financial literacy, one can often feel like a bewildered tourist trying to navigate a maze of stalls selling everything from overpriced trinkets to shiny gold bars. Fear not! Financial planning and investments can be your trusty map, guiding you through the intricacies of asset protection, credit management, and the thrilling world of currency trading—all while keeping your wallet happy and your credit score dancing.

Estate Plan Trusts and Asset Protection

An estate plan trust is not just a fancy piece of paper; it’s like your financial superhero, swooping in to protect your assets from the clutches of creditors. By placing your assets in a trust, you can mitigate credit risks and ensure that your wealth is passed on to your loved ones without the dreaded probate process.

“A trust is like a safe haven for your assets, shielding them from unpredictable storms.”

Consider this: if you own a home or investments, placing them in a trust means they are technically owned by the trust and not directly by you. This can provide protection from creditors attempting to seize your property to settle debts. It’s akin to wearing a superhero suit that makes your assets invisible to those pesky credit risks!

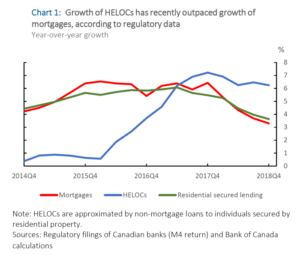

Home Equity Loans and Credit Management

Home equity loans can be a double-edged sword, offering the allure of quick cash while simultaneously posing risks to your credit score. When managing credit, it’s essential to understand the implications of borrowing against your home’s equity.Before diving into this financial pool, here’s a comprehensive guide on home equity loans:

1. Understanding Home Equity

Home equity is the difference between your home’s current market value and the outstanding mortgage balance. For example, if your home is worth $300,000 and you owe $200,000, your home equity is $100,000.

2. Loan Types

Home equity loans come in two flavors: fixed-rate loans and home equity lines of credit (HELOCs). Fixed-rate loans give you a lump sum with a consistent payment, while HELOCs provide a revolving line of credit that can fluctuate.

3. Credit Score Impact

Using a home equity loan can affect your credit utilization ratio. High balances can lower your score like a lead balloon, so it’s wise to borrow only what you need—no extravagant shopping sprees with your new-found cash!

4. Risks

If you default on a home equity loan, you risk losing your home. It’s like betting your house on a game of poker—only gamble what you can afford to lose.

5. Alternatives

Consider cheaper alternatives for financing, such as personal loans or even negotiating with creditors directly, to avoid putting your home on the line.

Currency Trading Essentials and Responsible Credit Use

Currency trading, while it may sound like an elite club for financial wizards, is actually a thrilling arena where anyone can join the fray. However, engaging in this market requires a solid understanding of responsible credit use.Before plunging into the world of forex trading, keep the following tips in mind:

Learn the Basics

Before risking your hard-earned money, familiarize yourself with currency pairs, pips, and leverage. The forex market is like an intricate dance—know the steps before you hit the floor!

Start Small

Begin with a demo account or a small amount to test your strategies. Think of it like dipping your toes into a pool before cannonballing in!

Set a Budget

Allocate a specific amount for trading and stick to it. This prevents you from overspending and keeps your credit score intact. Remember, it’s a marathon, not a sprint!

Use Leverage Wisely

Leverage allows you to control a larger position with a smaller amount of capital. It’s a bit like playing with fire; too much can lead to burns, but just the right amount can help you toast marshmallows of profit!

Stay Informed

Follow market trends and news that can impact currency fluctuations. Knowledge is your best weapon in the trading arena.

Avoid Emotional Trading

Making decisions based on emotions can lead to poor choices. Keep your head cool and your strategies sound; trading with a clear mind is like shooting fish in a barrel—much easier and less messy!

Ending Remarks

As we wrap up our adventure through the world of credit management, remember that avoiding credit mistakes doesn’t require a cape—just a keen eye and a willingness to learn! Whether you’re consolidating debt, planning for the future, or just trying to keep your credit score from doing the limbo, there’s a wealth of knowledge at your fingertips. So go forth, fellow financial hero, and let your credit story be one of triumph!

Expert Answers

What are common credit mistakes to avoid?

Common mistakes include late payments, maxing out credit cards, and applying for too many loans at once.

How can I improve my credit score quickly?

Pay down high credit card balances, ensure all bills are paid on time, and avoid new hard inquiries.

Is credit counseling worth it?

Yes! Credit counseling can provide personalized strategies and support to improve your financial health.

What’s the difference between debt consolidation and debt settlement?

Debt consolidation combines multiple debts into one loan, while debt settlement involves negotiating to pay less than what you owe.

How often should I check my credit report?

It’s wise to check your credit report at least once a year to catch errors and monitor your score.