Loan relief isn’t just a fancy buzzword tossed around at cocktail parties—it’s the golden ticket to your financial freedom! Imagine a world where your debts don’t haunt you like a ghost in a horror movie, and that’s exactly what these loan relief programs aim to achieve. From navigating the maze of eligibility criteria to applying for assistance, this guide is your trusty map through the enchanted (and sometimes confusing) forest of debt management.

Whether you’re drowning under a mountain of loans or just trying to keep your financial ship afloat, understanding the various types of loan relief programs can turn the tide in your favor. So grab your life vest and let’s dive into the deep waters of debt management strategies, financial planning, and the elusive treasure of loan relief!

Loan Relief Programs

Navigating the world of loans can feel like trying to find your way out of a corn maze while blindfolded. Fear not, brave borrower! Loan relief programs are here to guide you through the twists and turns, offering a helping hand when the debt becomes too overwhelming. These programs are designed to ease your financial burdens, and understanding them can be the first step toward financial freedom.Loan relief programs come in various shapes and sizes, catering to different needs and situations.

From federal initiatives aimed at students to local programs for small businesses, there’s likely a program designed just for you! Here’s a deeper dive into the types available, eligibility criteria, and the application process to get you on the path to relief.

Types of Loan Relief Programs

Diverse loan relief programs exist to help borrowers tackle their unique financial dilemmas. Here are some common types:

- Student Loan Forgiveness: A glimmer of hope for graduates feeling crushed by student loan debt. Programs like Public Service Loan Forgiveness allow borrowers in qualifying jobs to have their loans forgiven after making a set number of payments.

- Mortgage Forbearance: This temporary relief allows homeowners to pause or reduce their mortgage payments during financial hardship, providing a much-needed breather.

- Debt Consolidation Programs: These programs help you combine multiple loans into one single payment, often at a lower interest rate, simplifying your repayment process and reducing stress.

- Business Loan Relief: Designed for small businesses, these programs offer grants or low-interest loans to help them survive economic downturns, ensuring they can keep their doors open.

Eligibility Criteria for Loan Relief Options

To access these life-saving loan relief options, borrowers must meet specific eligibility criteria that can vary widely depending on the type of program. Understanding these requirements is crucial for getting the help you need:

- Income Level: Many programs target low to moderate-income borrowers, so demonstrating financial need is often a requirement.

- Loan Type: Eligibility can depend on the type of loan you have, as federal programs often focus on federal loans rather than private ones.

- Employment Status: Some programs, especially for student loans, require you to be employed in specific sectors or roles, such as public service or teaching.

- Payment History: A solid payment history can enhance your eligibility for certain programs, while a history of missed payments may complicate matters.

Application Guide for Loan Relief Assistance

Applying for loan relief assistance can feel like preparing for a first date—nervous, but ultimately rewarding! Here’s a step-by-step guide to help you navigate the process smoothly:

- Research Programs: Start by investigating the various loan relief programs available to determine which ones you qualify for. Each program has its own unique flavor, like a buffet of options.

- Gather Documentation: Compile necessary documents such as income statements, loan details, and proof of hardship. Think of it as creating your financial portfolio for a prestigious art gallery.

- Fill Out Applications: Carefully complete the applications for the programs you’ve chosen. Ensure all information is accurate, avoiding the temptation to embellish your “impressive” financial history.

- Follow Up: After submitting your applications, follow up to confirm receipt and check the status. Sometimes, a polite nudge is all it takes to speed things along.

“Financial freedom is available to those who learn about it and work for it.” – Robert Kiyosaki

Debt Management Strategies

Managing debt can sometimes feel like trying to juggle flaming swords while riding a unicycle on a tightrope. Fear not, weary borrower! With the right strategies in your arsenal, you can tame the wild beast of debt and emerge victorious. Let’s dive into some effective debt management techniques that can help reshape your financial landscape while keeping your sense of humor intact.Effective debt management strategies are akin to a superhero armor for your finances.

They can empower borrowers to take control and navigate the treacherous waters of loans and debts. Here’s a breakdown of some strategies, complete with a step-by-step plan for debt consolidation and the invaluable role of credit counseling.

Debt Consolidation Steps

Imagine consolidating your debts as if you were merging all your favorite flavors of ice cream into one delicious sundae. Instead of juggling multiple bills, you get one smooth, creamy payment (with sprinkles, of course). Here’s how to go about it:

1. Assess Your Debt

Gather all your bills, loans, and outstanding balances. It’s like assembling the Avengers; you need to know who you’re dealing with.

2. Research Consolidation Options

Look into personal loans, balance transfer credit cards, or debt management plans. Each option has its own set of superpowers.

3. Choose a Suitable Option

Pick the superhero that best fits your needs—consider interest rates, fees, and terms. Remember, even superheroes have to read the fine print.

4. Apply for a Consolidation Loan

If you choose a loan, apply for it and wait for approval. This is where your financial diligence pays off.

5. Pay Off Existing Debts

Use the funds from your consolidation loan to clear your debts. Voilà! You’ve defeated the villain!

6. Create a Budget

Develop a budget that factors in your new monthly payment. No more spending like a kid in a candy store!

7. Stay Consistent

Stick to your payment plan. Consistency is key, just like Bruce Wayne’s nightly training sessions.

The Role of Credit Counseling

Credit counseling serves as your financial GPS, guiding you through the confusing maze of debt management. These professionals can help you understand your financial situation, create a budget, and develop a debt repayment plan. Here’s how credit counseling can benefit you:

Personalized Financial Assessment

Credit counselors conduct a thorough analysis of your finances, identifying areas for improvement and strategies tailored to your situation.

Debt Management Plans

Counselors can help set up a Debt Management Plan (DMP), allowing you to consolidate payments into one monthly fee. It’s like having a financial fairy godmother who waves a wand and simplifies your debts!

Negotiating with Creditors

With their expertise, credit counselors can negotiate lower interest rates or waived fees on your behalf, which is akin to having a seasoned diplomat working to ease financial tensions.

Financial Education

Beyond just managing debts, credit counseling provides valuable education on budgeting, saving, and rebuilding credit, empowering you to make better financial choices in the future.In the world of debt management, knowledge truly is power. By implementing these strategies and seeking guidance from credit counselors, borrowers can navigate their financial journeys with confidence and a hint of humor, turning what once felt like a chaotic mess into a well-orchestrated symphony of financial harmony.

Financial Planning and Recovery

In the whimsical world of finance, creating a robust financial plan is akin to wearing a superhero cape—essential for overcoming the villainous threat of loan issues! Think of your financial plan as your trusty sidekick, ready to assist you in navigating through the treacherous waters of debt. With a little foresight and a sprinkle of motivation, you can become the hero of your financial story.To avoid future loan predicaments, it’s crucial to craft a plan that’s as sturdy as the foundation of Fort Knox.

Not only does this involve budgeting and tracking expenses, but also preparing for unforeseen circumstances that could throw your financial ship off course. Let’s dive into some key strategies that can help solidify your financial future.

Tips for Creating a Robust Financial Plan

Having a detailed financial plan is like having a GPS for your money; it keeps you on the right track. Here are essential tips to bolster your financial defenses:

- Set Clear Budget Goals: Establish a budget that Artikels monthly income and expenses. Track your spending as meticulously as a squirrel hoarding nuts for winter.

- Build an Emergency Fund: Aim for three to six months’ worth of living expenses. Think of it as your financial airbag—always there to cushion the blow of unexpected bumps!

- Prioritize Debt Repayment: Use the avalanche or snowball method to tackle debts. The avalanche method saves you interest, while the snowball method gives you quick wins. Choose your superhero weapon wisely!

- Review and Adjust Regularly: Life changes, and so should your financial plan. Regular check-ups help you stay in tune with your financial health and adapt to changes in income or expenses.

Estate Plan Trusts and Asset Protection

When the financial storm clouds gather, estate plan trusts become your financial umbrella, shielding your assets from the downpour of financial hardship. Utilizing trusts in your estate planning ensures that your assets are protected and distributed according to your wishes. A trust can serve as a protective shield, maintaining control over who receives your assets and when. This is especially important during times of financial instability, as it helps safeguard your estate from creditors.

Here’s why incorporating trusts into your estate plan is a wise strategy:

- Asset Protection: Trusts can protect your assets from lawsuits or creditors, ensuring they remain secure and out of the reach of financial misfortunes.

- Controlled Distribution: You can stipulate when and how your heirs receive assets, preventing potential wild spending sprees—no one wants to fund a lavish llama farm!

- Tax Benefits: Certain types of trusts offer tax advantages, which can be beneficial during financial recovery periods.

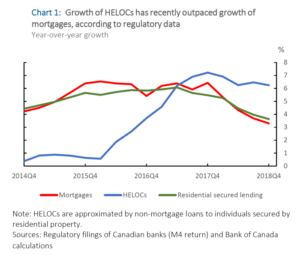

Home Equity Loans in Loan Relief Scenarios

Home equity loans are like the Swiss Army knives of financial tools—versatile, handy, and ready to get you out of a jam! When facing loan difficulties, tapping into your home equity can be a smart move. But before you dive headfirst, let’s unpack the benefits of this approach.Home equity loans enable homeowners to borrow against the value of their home, providing access to cash for various needs.

Here’s a guide to understanding how these loans can help in loan relief scenarios:

- Lower Interest Rates: Home equity loans typically offer lower interest rates compared to personal loans and credit cards, making them a more affordable option for borrowing.

- Fixed Payments: Enjoy predictable monthly payments with fixed rates, allowing for easier budgeting and planning—no surprises like finding an extra sock in the laundry!

- Tax Deductibility: Under certain conditions, the interest paid on a home equity loan may be tax-deductible, which can provide financial relief during tax season.

In summary, crafting a solid financial plan, utilizing estate plan trusts, and considering home equity loans are powerful strategies for navigating the financial labyrinth. With these tools in your arsenal, you’ll be well-equipped to tackle future loan challenges and emerge victorious!

Final Summary

So there you have it—your epic quest for loan relief explained! With a treasure trove of information on programs, strategies, and recovery plans at your fingertips, you’re well-equipped to slay the debt dragon and reclaim your financial kingdom. Whether you choose to consolidate your debts like a savvy wizard or embark on a financial recovery journey, remember: loan relief is the magical spell that can help turn your fiscal misfortunes into a happily ever after!

Q&A

What are the main types of loan relief programs?

The main types include deferment, forbearance, and loan forgiveness programs, each designed to ease the burden of debt in different situations.

Who qualifies for loan relief programs?

Eligibility often depends on factors like income, type of loan, and financial hardship, but it varies by program.

How do I apply for loan relief assistance?

Start by contacting your lender or checking official websites for specific application processes and required documentation.

Will loan relief impact my credit score?

It can, but it depends on the type of relief you receive; some programs may temporarily affect your score, while others do not.

How can credit counseling help with loan relief?

Credit counseling can provide personalized plans and strategies for managing debts, leading to better chances of qualifying for relief.